What is mortgage insurance?

Mortgage insurance covers your mortgage payments in the event of serious illness, disability or death. It is a product often recommended by the financial institution providing your mortgage in order to insure against these three risks. The mortgage lender can require mortgage insurance (which is rare), but they cannot require you to take it from them. They must leave you free to choose your insurer. It’s also important to know that the lender’s insurance can be cancelled at any time without penalty. And no, you don’t have to wait for the renewal of your term to cancel your insurance. However, are you truly well informed about the details of getting mortgage insurance from your financial institution? Analysis shows that this type of insurance product is definitely not the best option to protect you. In many cases, a personal insurance policy is a less expensive and more advantageous solution.

Here are a few advantages of taking out a personal insurance policy:

• You – and not the financial institution – are the policy owner

If you decide to change the financial institution for your mortgage, you don’t have to provide new proof of insurability since your policy is not linked to your loan. This enables you to retain your power of negotiation in the event of a health problem that could make you non-insurable; you are therefore not obliged to stay with your lender and you can still get the best mortgage rates. That’s something to think about.

It’s also possible to make a change to your insurance. The mortgage insurance that we offer includes the important advantage of flexibility to adjust the type and amount of your insurance, and even transform it into a permanent life insurance policy, without any proof of health status!

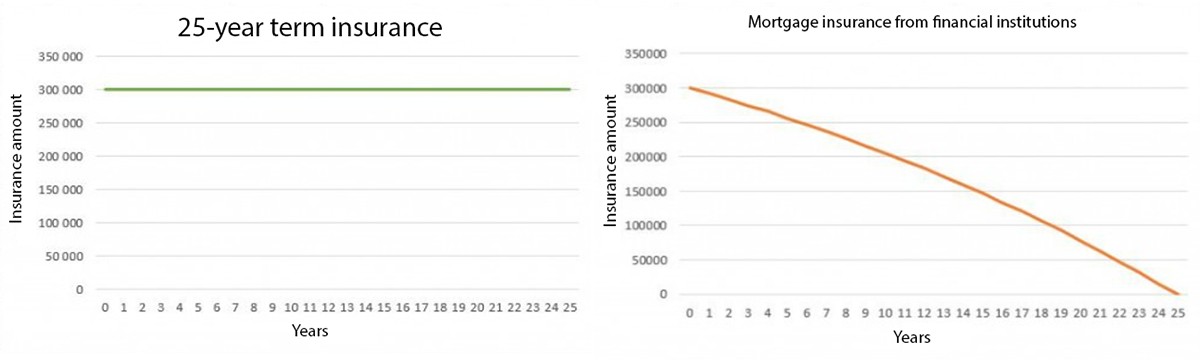

• You receive fixed protection for the duration of the policy

Unlike what happens with a mortgage from a financial institution, your financial protection does not diminish as you reduce your mortgage balance. Regardless of your mortgage term, we can offer you fixed insurance that will not decrease in tandem with your mortgage balance. Your mortgage insurance premium is therefore guaranteed for the duration chosen at the outset (10-, 15-, 20-, 25-, 30-year term, etc.).

• You choose the beneficiaries

In the case of mortgage insurance products from financial institutions, the institution is automatically the beneficiary. Under a personal insurance policy, on the other hand, the beneficiaries of your choice can use the insurance payout as they wish – to pay off the mortgage balance, invest the amount, or even finance a building renovation or other project.

• Personal insurance is less expensive

Mortgage insurance is generally expensive and highly profitable for financial institutions. This type of insurance does not differentiate between a non-smoker in good health and a smoker in poorer health. With personal insurance, many of your personal attributes (such as gender, smoker/non-smoker, occupation, lifestyle, age, health condition and medical history) are factored in. This means that people with favourable factors can obtain much lower premiums.

We are “ your ” avisor

As “your” advisor, we take your interests into account, and look at many insurance companies to find the most suitable solution for your situation and needs, at the best possible rate. Contact us for a free consultation. Who knows, you might be pleasantly surprised!

Still sceptical? View this short video in which Pierre-Yves McSween clearly summarizes the advantages of getting term insurance, as opposed to mortgage insurance from your financial institution.